We believe you can go further and do more when you have a trusted risk-discussion partner on your team, who will look at your business holistically to uncover new opportunities.

We are a leading global reinsurer that helps insurance companies reduce their earnings volatility, strengthen their capital and grow their businesses through reinsurance solutions.

An automated underwriting system can help increase underwriting efficiency and consistency, reducing operational costs and the time required to issue a policy, and critically, it can improve customer satisfaction for sales growth.

Several systems are available in the market. To help you research beyond a provider’s high-level content and demos to evaluate the right system for your business, we recommend asking them the following five questions.

Q1. What level of underwriting automation can reasonably be achieved in your target market?

Why is this question important? A straight through processing (STP) rate refers to the ability of the system to automatically underwrite without manual intervention. Without proper context, however, STP rates can be misleading. This is because marketed STP rates are often based on relatively straightforward risks, products and other business parameters. It’s essential to understand what was used and to validate if this fits with your unique requirements. We recommend asking:

On what exact basis were the STP rates calculated and are these in line with your target market? For example:

What type of underwriting process was involved; were the risks pre-triaged so that only simple risks were directed through the system?

Is the STP rate calculated at an assured life level, application level or on a particular (e.g. Death) benefit?

Is asking for more evidence and/or referring for manual underwriting considered to be STP?

What is the STP rate when a living benefit, e.g. Critical Illness, is applied as a rider to the main benefit?

For what market/s and distribution channel was the system designed?

How does the customer’s underwriting journey align to your brand/desired customer experience?

Q2. How reliable are the underwriting rules and what’s the process for keeping them current?

Why is this question important? Underwriting rules are never static, as COVID-19 has highlighted. Changes in risk must be reflected in underwriting philosophy on an ongoing basis. We recommend asking:

Where does the underwriting expertise come from?

As more risk data becomes available, are the rules updated and is there a commitment to R&D?

Is it possible to customize the rules to your underwriting philosophy and risk management framework? If so, what’s the process for this, how long does it take and what resources are required from your company?

On an ongoing basis, if you want to make changes to the rules or customer journey, how quickly can these changes be applied?

Q3. Will it enable continuous improvement to your product/s and customer experience?

Why is this question important? The key to continuous improvement is access to real-time data insights. We recommend asking:

Does the system offer built-in analytics?

Is there a user-friendly interface for accessing reports?

Can business users easily create and access customized reports?

Would the available analytics enable business users to identify friction points in the underwriting journey?

Can the analytics support A/B testing?

Q4. Is the implementation model right for your organization?

Why is this question important? The model for a system’s delivery – i.e. software as a service (SaaS) or on-premises – impacts integration, updates and maintenance, as well as aspects that could become more important over time as your business evolves. SaaS models, for example, tend to have limited customization potential. On-premise models often can’t be scaled-up easily, an issue if you’re considering expanding into new markets or products. We recommend asking:

For SaaS models, what level of customization is possible?

For on-premise models, can the system be scaled up quickly?

How are updates and upgrades managed?

Where is the data stored, how is it kept secure and what is in-place to prevent unauthorized access?

Will the model integrate easily with your existing IT systems?

Q5. What is the total cost of ownership?

Why is this question important? Total cost of ownership is the sum of all direct and indirect costs. While upfront implementation costs and license fees are often well defined, costs for maintenance, customization and internal effort may be underestimated and will need to be managed. We recommend asking:

What are the different cost components, e.g. for licensing, maintenance and support?

What maintenance and support services are covered by fixed costs and what will be charged on a variable (consumption) basis?

What internal IT resources are required to support the integration process?

What internal underwriting resources are required to support the system?

What is the cost of interfacing with an external system, if needed?

How long does it take to train a new business user?

What are the termination conditions?

What is the cost of adding a new product and entering a new market?

What is the cost for an upgrade or enhancement, e.g. to build a new functionality?

Is there an additional cost for disaster recovery and high availability?

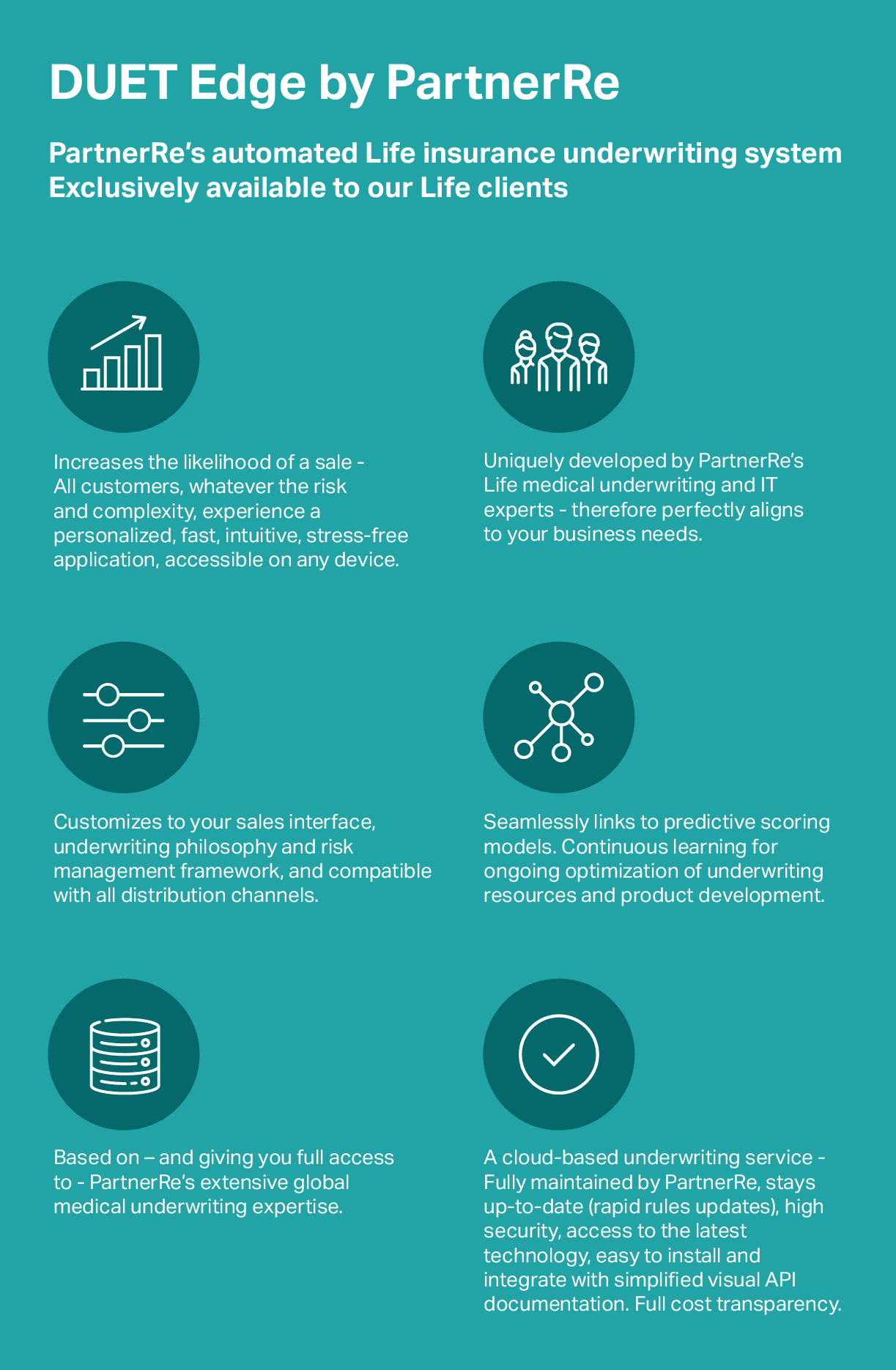

PartnerRe’s automated Life insurance underwriting system

We hope you find these questions helpful.

Please contact us – details below – to ask how our automated Life underwriting system, DUET Edge by PartnerRe, performs in all these respects.

The above descriptions of DUET Edge by PartnerRe are meant for illustration purposes only; the actual use / licensing of the DUET Edge product is governed by the applicable terms and conditions with PartnerRe.