We believe you can go further and do more when you have a trusted risk-discussion partner on your team, who will look at your business holistically to uncover new opportunities.

We are a leading global reinsurer that helps insurance companies reduce their earnings volatility, strengthen their capital and grow their businesses through reinsurance solutions.

Looking at historical losses, 2017 and 2018 were outlier events. Correct? Well “Yes and No”! The loss data says “Yes” – the industry hasn’t seen such severe losses before. In contrast, our CatFocus® California Wildfire model says “No” – it shows that several similar wildfire events have occurred over the last half century.

Ergo, if your risk assessment is based only on industry loss data, you’re not getting the full picture. It’s time for a rethink.

We explain the losses vs model discrepancy and recommend a more robust approach to assessing and managing portfolios exposed to California wildfire.

Executive summary

The 2017 and 2018 industry losses were the most severe since 1950, but were in fact not that unexpected given the loss potential of other historical events.

The industry should be prepared for future losses of a similar magnitude to 2017 and 2018, and at return periods which will significantly impact property portfolios.

Our estimated return period of a USD 10 billion annual aggregate industry loss is 20 years.

Exposure growth, especially in areas close to wildland, is the main driver of the changing risk landscape for California wildfire. It explains why regions with no prior loss are now also at risk.

Other factors impacting wildfire risk include human activities, weather, climate variability, climate change and biosphere-climate interactions, some of which are changing over time.

Risk assessment based on historical loss records alone cannot therefore reliably quantify this risk. A catastrophe model is the only viable method. The CatFocus® model provides a reliable benchmark view of California wildfire risk.

The CatFocus® model shows clear differences between Northern and Southern California1:

The annual aggregate losses of 2017 and 2018 were the most extreme years for Northern California. For Southern California, the losses from these years were not uncommon and were comparatively far less extreme.

Compared to Southern California, severe losses in Northern California have a greater contribution to the annual aggregate expected loss of California as a whole.

Susceptibility to wildfire is lower in the south than in the north, due to different fuel types, fire spread and fire suppression aspects.

Reported and modeled losses give very different estimates of risk

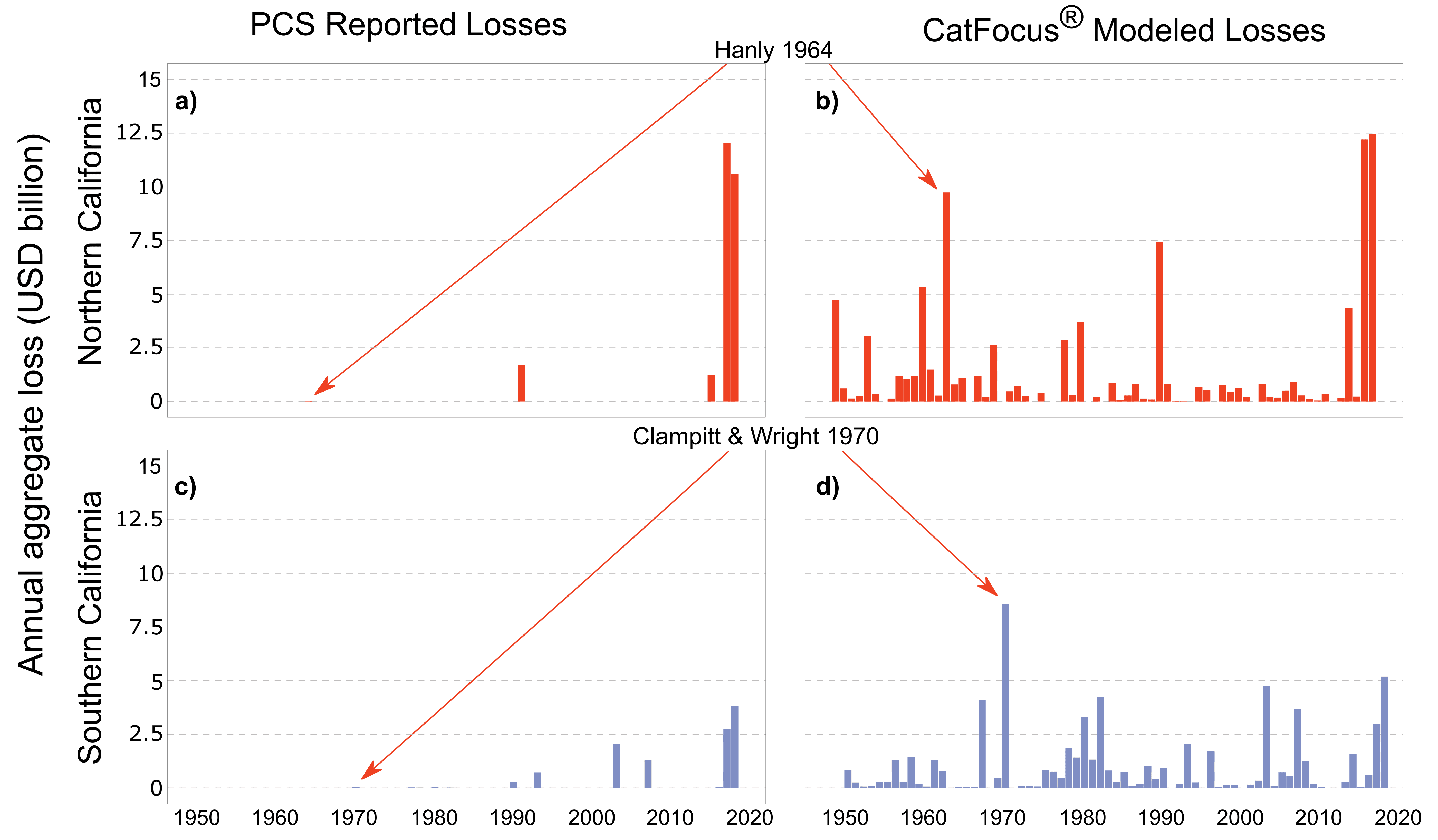

Reported losses California wildfire risk assessment based on reported industry losses (see figure 1a & 1c, PCS recorded industry losses from 1950 to 20182) indicates that the 2017 and 2018 losses were extreme, especially in Northern California. There are many years in the 1950 to 2018 time period when no losses exceeded the PCS’s reporting threshold3.

PartnerRe’s catastrophe model In contrast, results from PartnerRe’s CatFocus® California Wildfire catastrophe model (see figure 1b & 1d) indicate that, using current industry exposure, many years in fact had the potential for losses greater than the PCS threshold. Previous historical events could have led to losses comparable to or exceeding the magnitude of loss observed in Northern and Southern California in 2017 and 2018 (figure 1a & 1c).

The difference is mainly due to changes in where people are living.”

Figure 1: Annual aggregate reported industry losses in USD billion for (a) Northern and (c) Southern California. Source: PCS2. Modeled annual aggregate losses for (b) Northern and (d) Southern California. Source: CatFocus®, PartnerRe. The difference between reported and modeled loss is significant – see also the disparate loss estimates for the Hanly (1964) and Clampitt & Wright (1970) wildfires – and strongly speaks to using robust catastrophe models to assess and evaluate current California wildfire risk. The PCS losses are only those that were reported and which caused an industry loss above the PCS loss threshold3. To ensure comparability with the reported losses, the same (current PCS) threshold is used for the modeled losses.

Why are these two estimates of risk so different?

The difference is mainly due to exposure growth: changes in where people are living (e.g. from 1990 to 2010, the number of buildings in the Wildland-Urban Interface4 increased from 3.3 to 4.4 million5), higher population density and increased property values. This exposure growth has a particularly strong positive and complex (non-linear) impact on risk evaluation.

Risk assessments informed by reported losses (which also often have the issue of incomplete loss record due to reporting biases) are challenged to adequately and reliably take exposure growth and other risk factor changes into account. In contrast, catastrophe models can do this well and therefore lead to a different estimation of the risk.

Modeled return periods of the 2017 and 2018 annual aggregate losses

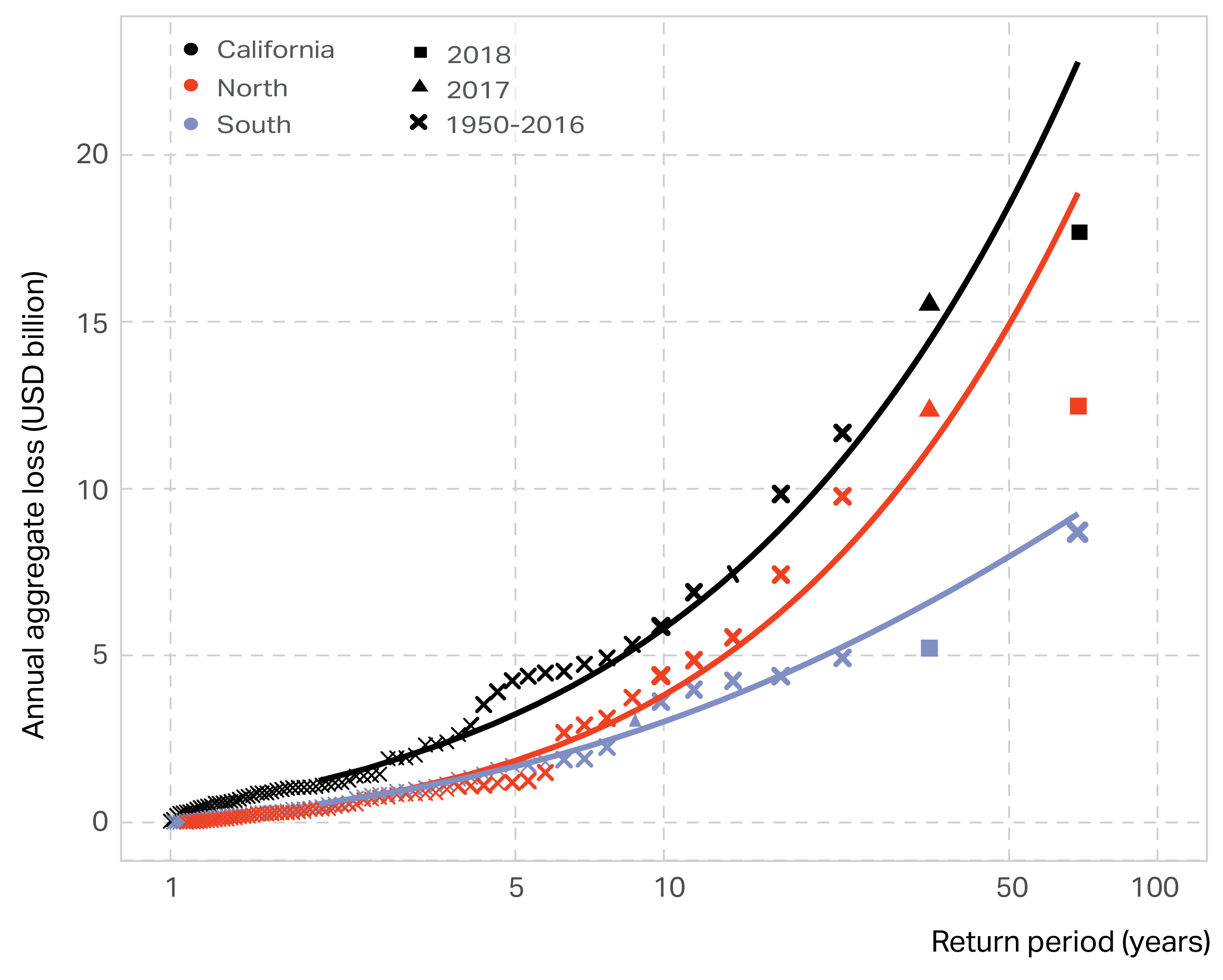

Figure 2 shows the model’s derived annual aggregate exceedance probability curves for California, and for the Northern and Southern California regions; to aid interpretation, we fitted smoothed curves to the individual annually aggregated modeled losses.

Figure 2: Modeled industry annual aggregate loss exceedance probability curves for California as a whole, Northern California and Southern California. The 2017 (triangles) and 2018 (squares) annual aggregate losses for each region are also shown. Return periods of the modeled losses (crosses) are calculated using the empirical method, where the highest modeled loss has a return period of 69 years, equal to the length of the modeled time series shown in figure 1b & 1d. The smoothed colored lines are generalized extreme value distributions fitted to each regions’ modeled losses. Source: CatFocus®, PartnerRe.

For California as a whole, CatFocus® indicates that:

the estimated return period of a USD 10 billion annual aggregate industry loss is 20 years

the estimated return period of a USD 15 billion annual aggregate industry loss, close to the reported PCS loss value for 2017, is 35 years.

For Northern California, CatFocus® indicates that 2017 and 2018 annual aggregate losses:

are extreme with respect to the period 1950-2018

are comparable in modeled loss magnitude to historical wildfire events in 1991 and 1964 (see figure 1c)

have estimated return periods of 40 years.

Our estimated return period of a USD 10 billion annual aggregate industry loss is 20 years.”

In addition, our own analysis points to a strong underlying positive trend in the hazard in this area over the last decade, which may be partly driven by other factors including climate change6,7,8. Modelled results require an adjustment to reflect this, and this adjustment further reduces the estimated return periods of the 2017 and 2018 losses.

For Southern California, CatFocus® indicates that:

2017 and 2018 losses have much shorter return periods than Northern California, of approximately 10 and 25 years respectively

there are multiple years with the potential to have caused losses equal to or greater than the losses observed in 2017 and 2018 (e.g. 1970, 1982, 2003 and 2007, see figure 1d), given current exposures.

Notable variation between insurance portfolios

The model allows us to differentiate the risk between different insurance portfolios – to reflect their specific exposure concentrations – and to ascertain portfolio-specific return period ranges for the 2017 and 2018 events (see table 1). Importantly, since there are a large number of potential loss events based on historical footprints, the model is able to identify at-risk regions that have not recently been loss affected.

Portfolio

Northern California

Southern California

2017

2018

2017

2018

Industry exposure

40

40

10

25

A

50

40

4

15

B

30

5

10

30

C

30

15

8

15

Table 1: Modeled return period estimates (in years) for the annual aggregate losses from the 2017 and 2018 events split by region, for the industry exposure and for three sample insurance portfolios. Source: CatFocus®, PartnerRe.

The CatFocus® California Wildfire Model

Developed by PartnerRe’s catastrophe research, modelling and underwriting experts, the CatFocus® California Wildfire model is a robust catastrophe model which captures the most important factors impacting wildfire risk; namely exposure change, hazard and the broad-scale vulnerability of typical insured residential and commercial property.

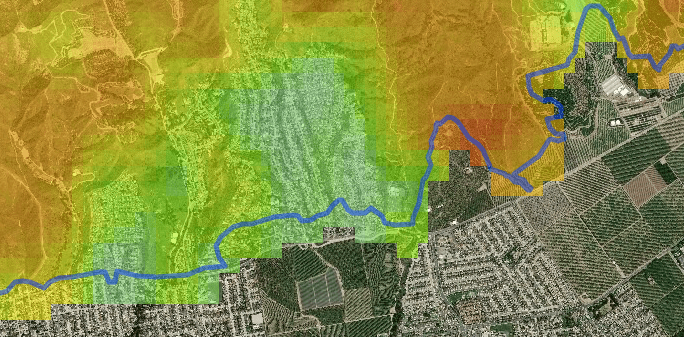

Model specifics The hazard component is based on historical fire perimeters compiled by the Fire and Resource Assessment Program (FRAP)9 from 1950-2018 for area burned exceeding 300 acres and conditioned with USDA wildfire hazard potential data10. See example footprint in figure 3. To estimate the ground-up loss, the model combines the hazard with high-resolution exposure information and an estimate of the damage ratio. The CatFocus® financial model then applies the re/insurance financial conditions to calculate the net loss.

Since historical losses show that the damage ratios in Northern California are in general higher than in Southern California, the model defines Northern and Southern California as two distinct vulnerability regions.

Figure 3: Example of a wildfire hazard footprint. Transect taken from the Thomas 2017 event in Southern California. The blue line is the FRAP9 fire perimeter and the colors indicate the wildfire hazard potential10 (red shaded areas have the highest potential). The property exposure can be seen in the background satellite imagery. Source: CatFocus®, PartnerRe11.

The model is able to reproduce the 2017 and 2018 industry losses (see figure 1b and 1d) and has been validated on insurer specific losses, a further indication that it is a reliable tool for risk assessment.

Limitations and developments The model considers the direct impact of fire within the fire perimeter and does not attempt to explicitly incorporate losses from indirect causes of damage, e.g. by smoke outside of the historical fire perimeters.

The model is limited to historical scenarios and does not yet include a “stochastic event set”, which would allow the model to be used for less homogeneous exposures. [Comment added September 15, 2020: “However, this is being added and will soon be available”].

There is uncertainty associated with using historical fire footprints overlaid on today’s exposure, summarized by the following question: Would the fire perimeter look the same given that there is now exposure within the footprint? We would expect that in some cases the historical fire would now be fought with different capabilities, which could affect the loss potential of an individual event. However, as observed in 2017 and 2018, isolated conflagrations ignited by flying embers are extremely difficult to fire fight and have resulted in significant losses. Overall, this suggests that historical scenarios are suitable and reliable for assessing today’s risk.

Additional analysis (not shown) of the 1950-2018 Californian wildfire activity (based on FRAP data) indicates a clear upward trend in burned surface area per year, primarily involving forest areas in Northern California. The trend is not as strong in Southern California, where wildfire more often occurs in shrubland. This implies that the model’s “stationarity assumption” may require adjustment, and that the return period for 2017 and 2018 in Northern California is likely to be shorter than the model suggests. This, and other non-stationarity factors such as climate change6, climate variability7, forest health8, and human interactions12, will be investigated in subsequent research projects.

Contributors

Luca Weber, Senior Researcher, Catastrophe Research

Dr. Niklaus Merz, Researcher, Catastrophe Research

Dr. Paul Della-Marta, Head of Catastrophe Research

Contact us

If you found this overview interesting, and/or have related findings or opinions to share, please contact us. We look forward to hearing from you.

This article is for general information, education and discussion purposes only. It does not constitute legal or professional advice of PartnerRe or its affiliates.